The STOP67 campaign set out its strategy and policy objectives at a webinar on Wednesday, 28th April.

The STOP67 Campaign hosted the webinar in the wake of the successful campaign to repeal the legislation raising the pension age to 67. With the public consultation of the Pension Commission concluded and the Government awaiting their report, the discussion focused on the opportunity to create a fair and flexible pension system for all that would address income security, adequacy and choice for older people.

Hosted by NWCI, the webinar included inputs from Age Action, SIPTU, Active Retirement Ireland, INOU and SpunOut. Representatives of the main political parties, including Fianna Fáil, the Green Party, Sinn Féin, the Labour Party and the People Before Profit participated iln the webinar aong with a range of other organisations and interested groups.

Addressing Inequalities in Older Age

Unless care is taken to balance a wide range of public policies, there is a serious risk that reforms to the state pension will reinforce existing inequalities in society and worsen the situation of those who are already facing cumulative disadvantages. Pension reform must avoid compounding disadvantage and economic inequality.

Orla O’Connor, Director NWCI highlighted the pension injustice experienced by women when she said ‘There should be an end to discrimination in pensions particularly for women who have taken responsibility for caring, often unpaid, for others. Women often work part-time/intermittently, many unable to accumulate social security contributions needed for a decent income in retirement’. In 2010, the average pension income of women was only two-thirds the income of men (at €280 compared to €433). Fewer than 3 in 10 retired women (28%) receive a private or occupational pension compared to more than half of all men (55%).

Deputy Marc Ó Cathasaigh highlighted the equality issues in the Total Contributions Approach noting the impact on carers, who have taken time out of the workforce, which potentially reduces their social security contributions saying ‘if we value a caring society then we must attach a value to it’.

Deputy Gary Gannon talked about how we can and should raise our ambition in terms of the State Pension. He noted that there are a number of people who are excluded from the State Pension and how a universal pension presents a solution towards tackling cumulative inequality in older age.

Sustainability and Income Adequacy

The debate about security in retirement has sometimes been wrongly framed as just a mathematical problem of managing the cost of the state pension. But behind the statistics are the people whose lives have been badly affected by recent reforms and who are still anxious about their financial security in retirement which was highlighted by all the panellists.

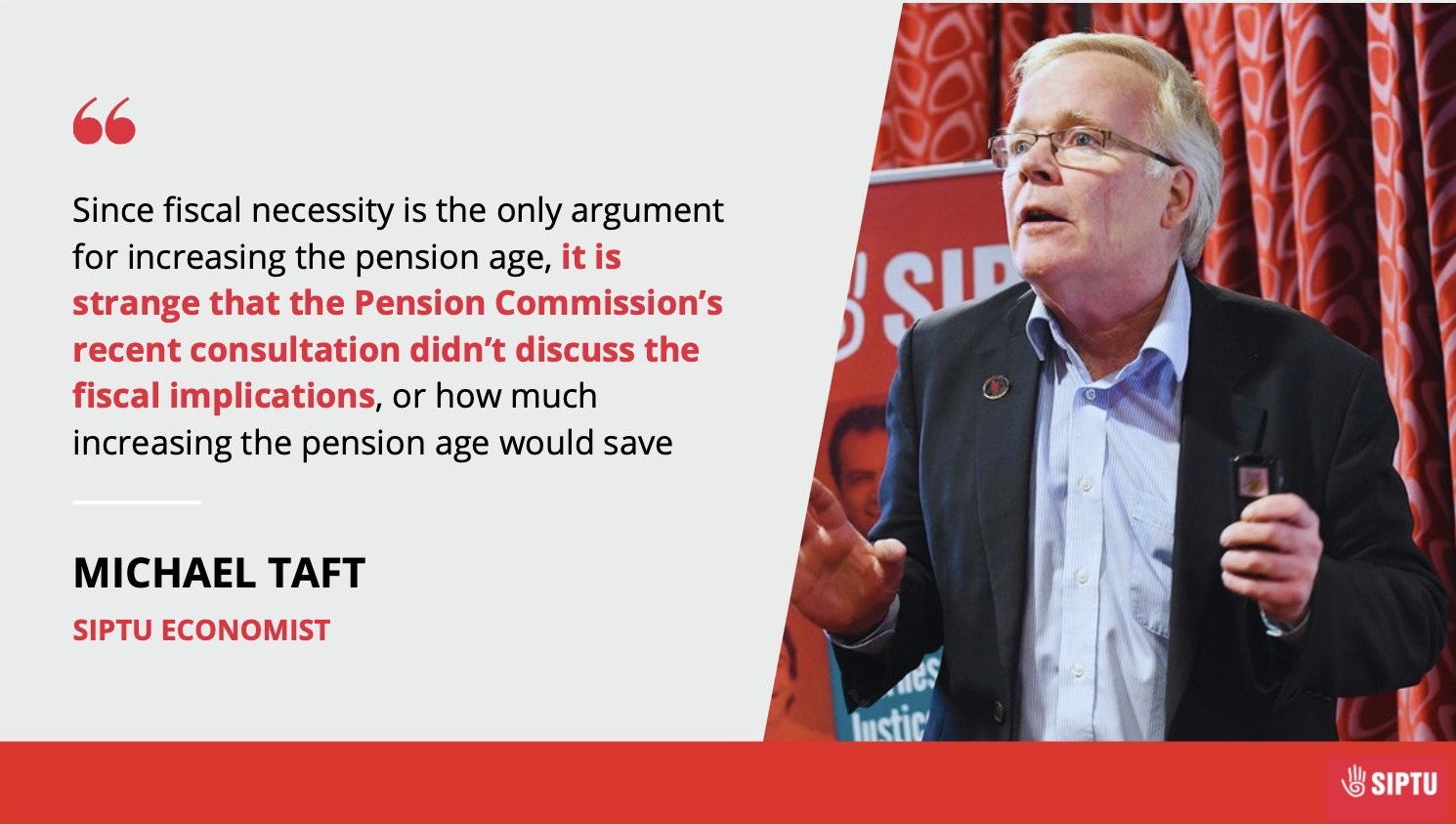

Challenging the fundamental assumptions about the savings that will be achieved by raising the pension age is something that needs to be continued Deputy Sherlock noted in his remarks which directly responded to the presnentation on fiscal sustainability of the pension by SIPTU's Micheal Taft.

Addressing the focus of debate on age eligibility Michael Taft said "Those arguing for increasing the pension age are actually kicking the can down the road. Increasing the pension age will save very little. They are avoiding real issues regarding pension sustainability – low employer PRSI and low growth."

Responding to the presentations Deputy Dara Calleary reflected on the fact that we need a broader conversation than just age and acknowledged that we need discussions to also focus on the social dimensions of pensions and fuller working lives.

Deputy Calleary’s comments are welcome given the assumption that older people close to and in receipt of, the State pension are generally mortgage-free home owners. It is clear that this is no longer true with many still carrying large mortgages, in mortgage arrears or living in precarious private rentals with no security of tenure in older age. Data released for the first time by the Central Bank of Ireland in 2019 showed over 20,000 over 50s were in mortgage arrears; over 7,000 of this number aged 60-69, over 2,000 aged over 70.

Deputy BrÍd Smith highlighted the poverty levels amongst people in receipt of the State pension and how important it is that income adequacy is established. Three-quarters of older people (75%) rely on the state pension as their main or sole source of income. There are serious concerns about the adequacy of the payment more than one in ten older people (10.5%) is at risk of poverty, and more than one in every nine (11.2%) experiences material deprivation.

Ireland needs an accurate picture of the cost of ageing in Ireland because without it, we do not know how State supports can best assist to lift people out of poverty and live with dignity in older age.

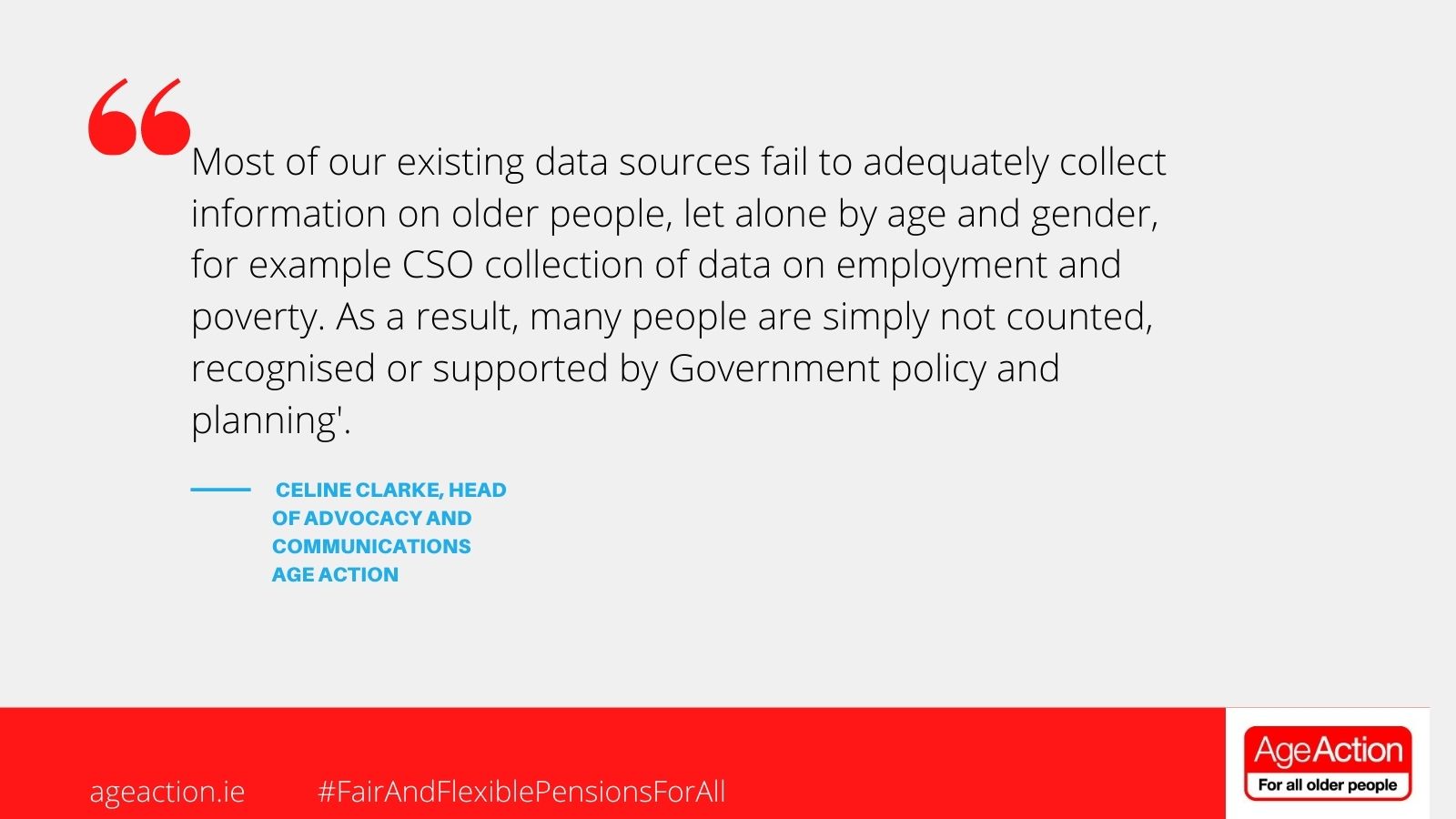

Most of our existing data sources fail to adequately collect information on older people, let alone by age and gender, for example CSO collection of data on employment and poverty. As a result, many people are simply not counted, recognised or supported by Government policy and planning.

Without such benchmarking data, it is difficult to plan a detailed approach to comprehensively meet the needs of vulnerable older people through the setting of appropriate pensions, secondary income supports and service provision. Age Action called for research on the cost of ageing ito inform Ireland’s policy development to meet the needs of an ageing population.

Ageism in the Workplace

Mandatory Retirement Clauses are part of the remit of the Pensions Commission.

Every year in Ireland older workers are forced out of their job for no other reason than they turn 65. This is possible because Irish law permits employers to impose mandatory retirement ages in their employee’s contracts, in effect, facilitating ageism and creating a set of second-class employment rights for older workers.

Deputy Louise O’Reilly and Deputy Sean Sherlock both voiced support for the abolishment of mandatory retirement clauses in private contracts. Deputy O’Reilly acknowledged the importance of giving people genuine choice to work longer if they chose to, in line with the choice afforded to people working in the public sector.

Ageist attitudes towards working later in life still exist, for example many older people have reported high levels of discrimination during recruitment. Before the COVID-19 pandemic three-quarters (75%) of those aged 55-64 who were unemployed were long-term unemployed (i.e. unemployed for more than one year). Research shows that becoming unemployed over 55 is generally a ‘one-way street’. Ireland has a higher than average rate of long-term unemployment for those aged 55-64 years.

Speaking about how people’s choice to work is undermined by such practices, Brid O’Brien of INOU said that ‘What needs to be addressed is ageism to ensure that people can work as long as possible and secure economic independence into their older age’.

Get Involved

In concluding the webinar Orla O'Connor urged the Pension Commission to listen to what the people of Ireland, as represented by Citizens Assembly, have told us about the kind of pension system they want - a system that allows all women and men to live with dignity & independence in their older years.

Participants were also encouraged to join the campaign through www.stop67.org.